The sustainable finance ecosystem is as vast and as complex as the overall finance sector that it is a part of. One way for data and service providers to understand the type of information this sector needs is to look at the different reporting standards and frameworks that the industry has created to standardise the sustainability related information it receives from corporates and investment projects. The bulk of these reporting initiatives are voluntary frameworks and cover sustainability related impacts and dependencies, but mainly focus on risks.

These reporting requirements are increasingly being translated into regulations. In 2015, France became the first country to introduce mandatory climate change related reporting for institutional investors. The European Commission is looking to integrate sustainability considerations into its financial policies and, in the UK, the Bank of England is a big advocate of better measuring and managing climate-related financial risks.

Within this article, we will give an overview of the most important and adopted voluntary reporting frameworks and the sections where geospatial data could provide inputs or add value.

Full financial disclosures in the face of climate change

A term that is often used within this context is ‘disclosure’. In the financial world, disclosure refers to the act of releasing all relevant information on a company that may influence an investment decision. This includes both positive and negative news, data, and other details about its operations, or details that impact its operations.

With climate change happening here and now, and impacting every sector of the economy, investors are becoming increasingly aware of the potentially large and detrimental impacts on the operational and financial performance of their investments. A better understanding of climate change risks and opportunities would allow corporates, investors, and regulators to better price climate risks and appropriately allocate capital.

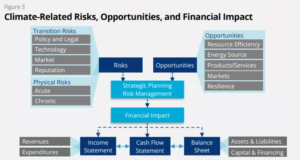

One of the most relevant and widely adopted initiatives on this front is the Task force on Climate-related Financial Disclosures (TCFD). The TCFD has developed a set of widely adopted recommendations that allow organisations to report climate-related information in their annual financial reports. The recommendations are voluntary and applicable for organisations across sectors and jurisdictions, and cover both climate change transition and physical climate change risks and opportunities. Specific recommendations are then developed around metrics and targets. Water, energy, land use, waste (management), and direct and indirect greenhouse gas emissions are recommended as specific metrics for disclosure, both in current and historic periods, to allow for trend analysis. Another recommendation is to use climate-related scenario analysis as a tool to understand the strategic and financial implications of climate-related risks and opportunities.

(Source: TCFD final report: Recommendations of the Task Force on Climate-related Financial Disclosures)

One of the main differences with some of the other sustainability and climate reporting frameworks listed below is the shift in emphasis from sustainability metrics only, to financial disclosures. Such as the impact of carbon regulation to consumer demand for a company’s products, or the supply chain disruptions likely to occur from severe weather events. More details on the actual recommendations, metrics, targets, and industry specific recommendations are publicly available in the TCFD Knowledge Hub.

Another relevant resource here is Acclimatise and UNEP Finance Initiative’s Navigating a New Climate report on piloting the TCFD recommendations around physical risks and opportunities across 16 banks. It includes two pilots with geospatial solutions and highlights the need for improved tools and spatial modelling expertise on the physical impacts of climate change for banks to better quantify physical risks and opportunities.

Sustainability reporting frameworks: more than climate risks

There are several other voluntary reporting guidelines and initiatives with a scope broader than climate change only. Major global initiatives include:

- United Nations Principles for Responsible Investment (UN PRI): The six Principles for Responsible Investment are a voluntary and aspirational set of investment principles that offer a menu of possible actions for incorporating Environmental, Social, and Governance (ESG) issues into investment practice. ESG issues that could be analysed with geospatial data include climate change, water, sustainable land use, fracking, methane, plastics, human rights and labour standards, and conflict zones. 1,567 investment managers, 406 asset managers and 264 service providers have signed up, representing over $80 trillion in assets under management or nearly a third of global wealth and investments.

- Carbon Disclosure Project (CDP): CDP runs a global disclosure system for investors, companies, cities, states, and regions to manage their environmental impacts. Companies, cities, and states disclose their climate change, deforestation, and water-related risks, CDP transforms this into detailed analysis and shares this with decision makers within businesses, investors, and policymakers. CDP has 525 institutional investors signed up with a combined $96 trillion assets under management and works with supply chains of 115 purchasing organisations and more than 11,500 suppliers.

- Sustainability Accounting Standards Board (SASB): SASB standards help businesses identify, manage, and report on the sustainability topics that are likely to affect a company’s financial or operating conditions most and are thus considered ‘material’. The standards are industry specific, as different industries will be more or less impacted by specific sustainability topics as highlighted in SASB’s Materiality Map. Categories that could be at least partially measured or analysed using geospatial data include greenhouse gas emissions, air quality, water management, waste management, ecological impacts, labour practices, and employee health and safety.

- Natural Capital Protocol (NCP): Natural capital is another term for the stock of renewable and non-renewable resources on our planet. Natural capital ‘assets’ include atmosphere, habitats, land geomorphology, minerals, ocean geomorphology, soils and sediments, species, and water. From these assets and stocks, ecosystem services flow providing economic, social, environmental, or cultural benefits to people. The NCP is a decision-making framework that enables organizations to identify, measure, and value their direct and indirect impacts and dependencies on natural capital. The 3rd stage of the protocol focuses on measuring and valuing natural capital, which is where geospatial data is most relevant.

Sustainability reporting challenges

The initiatives described above, alongside many other sustainability reporting frameworks, are not necessarily mutually exclusive and are often compatible with each other. The key for investors and companies preparing the reporting is to use the right framework for the right purpose and the right audience. Nevertheless, a lot of issues remain around sustainability and climate-related financial reporting. At a University of Cambridge conference on climate-related financial reporting, several challenges were highlighted:

- Current data underlying sustainability reports can be unreliable or incomplete. Reliable data on sustainability issues that is consistently available is needed to provide management and investors with the confidence to make decisions based on this information and reporting.

- There is still a gap of information between the policy and guideline level and what is actually being reported through company reports and disclosure.

- Tools are lacking that can value and quantify ESG and climate risks and impacts, that offer forward and backward analysis and that can be tailored for different sectors and geographies and their specific issues.

- Overall, information on the asset level (e.g. single factory, farm, hospital) is hard to come by or non-existent.

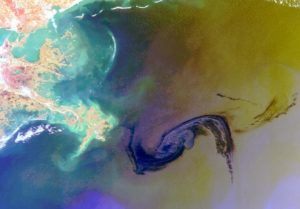

(The Deepwater Horizon oil spill in 2010 took 5 months to fully seal, discharged 4.9 million barrels of oil into the Gulf of Mexico causing extensive damage to wildlife habitats, fishing and tourism industries and cost British Petroleum over $42 billion. Image credits: ESA)

The geospatial data opportunity: complementing corporate reporting

So how can geospatial data, and satellite data in particular, play a role? Products and services based on geospatial data can add value in a number of ways to different stakeholders involved in the reporting and analysis processes:

- Satellite data could support the collection and aggregation of ESG information for corporates preparing their reports and disclosure according to the different reporting frameworks. Geospatial data can also serve as inputs into different scenario-modelling exercises.

- Companies can be reluctant to share information on certain types of risks. Whenever disclosure is not mandatory, they believe they could get penalised for reporting on risks that their competitors are simply not mentioning. Satellite data could provide a level playing field for both corporates and investors who are currently getting incomplete or no ESG information at all from their investees.

- Satellites can provide investors with ESG datasets that are comparable, complete, and consistently available, in parallel to corporate reporting. Compared to annual corporate reporting, satellite-derived ESG data could be updated more frequently to track progress and identify trends earlier on. There are opportunities for geospatial solutions to provide insights on the macro-, sector-, company- or individual asset level.

With the idea that ‘whatever is being measured, is being managed’, accurate, consistent, and comparable disclosure is needed for investors to effectively make more informed decisions to allocate capital to more sustainable and less risky investments. Although geospatial and satellite data are only one piece of the disclosure puzzle, they offer a highly complementary view to corporate disclosure because of its global scope, timely availability, and inherent comparability. So, let’s not wait until we have found the perfect indicators and data collection methods on ESG topics, let’s start now by developing innovative solutions to make geospatial data work for sustainable financial disclosure. There is a need, there is a market, and the UK is ideally placed to realise this opportunity and grow both the space and sustainable finance sectors simultaneously.

As part of the Catapult’s Explore Markets programme, we are investigating ‘Sustainable Finance’ as a growth opportunity for geospatial technologies. More information on Catapult’s activities in this area and some events where you can learn more about the topic and meet relevant players can be found on our website. More information on the sustainable finance sector, its key players and trends, and how they relate to the space sector can be found in the Catapult’s introductory paper.